£160bn lost as Coronavirus fears sees the FTSE suffer its worst day since 1987

Fears over coronavirus sparked the index’s worst day of trading in more than 30 years.

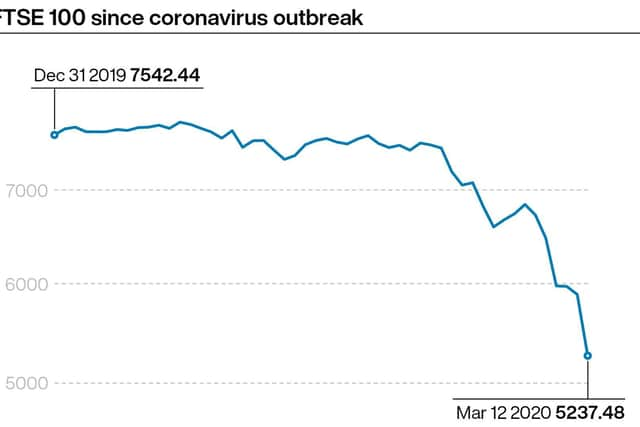

Investors ran scared from London’s shares as the index closed on Thursday down by 639.04 points to 5237.48 - the worst performance since 1987.

Advertisement

Hide AdAdvertisement

Hide AdThe 10.87 per cent fall is the biggest on London’s top index since October 20, 1987, the day after Black Monday, when the FTSE 100 fell 12.2 per cent.

It is also the second worst day in the FTSE’s history, ahead of the 10.84 per cent fall on Black Monday itself.

Croda, Morrisons and Persimmon - the three FTSE100 members which have the headquarters based in Yorkshire - all saw their share prices tumble.

Croda was down six per cent, Morrisons by 6.79 per cent and Persimmon by 11.99 per cent.

Advertisement

Hide AdAdvertisement

Hide AdThe UK’s listing of its 250 largest companies also had a terrible day, down 9.35 per cent.

It throws the index down to its lowest closing point since 2011.

It came after the World Health Organisation upgraded Covid-19 to a global pandemic, US President Donald Trump ended travel from Europe to the US, and the European Central Bank unveiled a package to tackle the infection’s effect on the economy which did not include interest rate cuts.

Spreadex analyst Connor Campbell said: “A horror show US open turned an already very bad day into the kind of session that could go down as historic, if for all the wrong reasons.

Advertisement

Hide AdAdvertisement

Hide Ad“It is hard to keep coming up with new metaphors for the scale of disaster facing the global markets.

“Equities are getting crushed under foot as investors flee to the fire exit, desperately scrambling about for safe havens that feel anything but.”

He added: “The ECB’s stimulus package seemingly only made matters worse.

“Withstanding the pressure to cut rates to a fresh record low, the central bank announced an 120 billion euro expansion to its ongoing quantitative easing programme, alongside new longer-term refinancing operations and cheap loans for banks to encourage lending to ‘those affected most by the spread of the coronavirus’.”

Even gold, typically a target for investors in times of crisis, fell by 4 per cent in value.