How one-in-four use money from families to buy their first home

Nearly a quarter of people in Britain rely on money from their families to buy their first home.

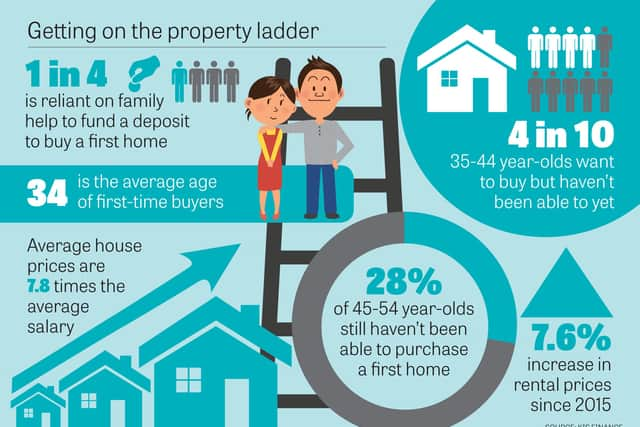

A recent report by KIS Finance has revealed that as people struggle to get on the property ladder, 23.5 per cent of Brits fund their deposits with help from their parents, or other family members.

Advertisement

Hide AdAdvertisement

Hide AdThe survey has also revealed how long people are having to wait before they are financially able to buy a house - often well beyond the average first-time buyer age of 34.

Graphic by Mark Hall

The survey's main findings showed:

23.5% of Brits have relied, or will rely, on financial help from members of their family to fund the deposit on their first home.44.2% of 35-44 year-olds want to purchase a house but haven’t been able to yet. Seventeen per cent of this group will be relying on help from family.28.3% of 45-54 year-olds still haven’t been able to purchase their first home and 7.6% of these will also be relying on help from family if they are ever going to get on the property ladder.

The report also looked at the potential reasons as to why so many prospective homeowners were having to rely on loans, gifts and inheritance from family to purchase their own home.

'Housing is becoming less affordable'

On average, house prices are 7.8 times more than the UK average annual salary. This figure has risen steadily over the last 20 years from 3.5 in 1997.

Advertisement

Hide AdAdvertisement

Hide AdLooking across the country, there are big regional differences. Buying a house in the North West of England will cost, on average, 2.5 times the average UK annual salary, while in London this figure rises to as much as 44.5 times for those buying in areas like Kensington and Chelsea.

'People are getting stuck in the rental cycle for longer'

In 2007 there were 2.8 million households in the private rental sector – by 2017, this figure had increased by 63 per cent to 4.5 million.

Rental households are also getting older, with the biggest increase being the number of 45-54 year-olds living in rented property which shows that more people are staying in the rental sector for longer and not able to purchase their first home.

With the overall number of people living in rented accommodation increasing, and rental prices having gone up by 7.6 per cent since 2015, experts say this may be a big contributing factor as to why so many people are having to wait longer to get on the property ladder.

Advertisement

Hide AdAdvertisement

Hide AdA further survey by KIS Finance looked at the reasons for being being declined mortgage applications.

Results included:

Income too low: 46.6%Unable to prove sufficient income (self-employed/contract worker): 34.1%Adverse credit history: 20.5%Lack of employment security: 15.9%Too many debts already: 13.6%Taken out a payday loan in the past: 8%Deposit too small: 13.6%

Eighteen to 24 year-olds represented the largest group of people who were declined a mortgage because of income with 62.5 per cent having been turned down for these reasons.

The second largest group in this category was 55-64 year-olds where 57.1 per cent of those who were declined a mortgage said it was because of income-related issues.

Advertisement

Hide AdAdvertisement

Hide AdResearch has shown that people in Britain are also relying on financial help from family to make purchases.Forty-five per cent of survey respondents said they had received help from family members to either purchase a car, or help cover its running costs.

The second most common reason for a family loan was to cover the costs of having children, including, initial costs of having a baby (buying prams, cots clothes etc.), childcare and school fees, with 34.4 per cent of our people saying they have received help for these reasons.

Nearly a quarter (22.4%) of respondents said they had received financial help from family to cover general day to day living expenses, including rent, bills and shortfalls in wages.